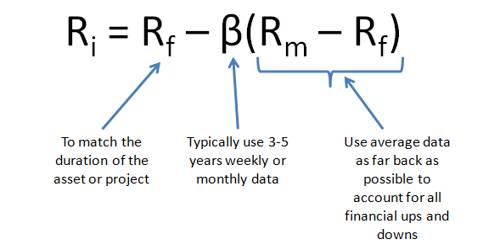

The capital asset pricing model (CAPM) provides a formula that calculates the expected return on a security based on its level of risk. The formula for the capital asset pricing model is the risk-free rate plus beta times the difference of the return on the market and the risk-free rate. Arbitrage pricing theory (APT) is a well-known method of estimating the price of an asset. The theory assumes an asset’s return is dependent on various macroeconomic, market and security-specific factors.

Differentiate between Arbitrage Pricing Theory (APT) and Capital Asset Pricing Theory –

The context of differentiation is given below:

CAPM

- It means the capital asset pricing model.

- CAPM is based on an investor’s portfolio demand and equilibrium arguments.

- It is based on risk-return trade-off.

- It is difficult to find a good proxy for market return.

- It has a simple beta.

- CAPM is a single factor model.

- CAPM requires that the market portfolio be efficient.

- CAPM assumes that the probability distributes of asset returns are normally distributed.

APT

- It means arbitrage pricing theory.

- APT is based on the factors model of returns and the approximate arbitrage arguments.

- It is based on mathematical and statistical data theory.

- It is difficult to identify approximate factors.

- It has several relevant data.

- APT is a multifactor model.

- There is no special role in the market portfolio in APT.

- APT does not make any assumption about the distribution of asset returns.

These are the context of differentiation between CAPM and APT.