The comparing step determines the degree of variation between actual performance and standard. If the first two phases have been done well, the third phase of the controlling process – comparing performance with standards – should be straightforward.

Comparing Actual Performance with Standards

This step involves a comparison of actual performance with the standard. Such a comparison will reveal the deviation between actual and desired results.

The comparison becomes easier when standards are set in quantitative terms. For instance, the performance of a worker in terms of units produced in a week can be easily measured against the standard output for the week.

Comparing Performance against Standards

- Performance may be higher than, lower than or identical to the standard.

- The timetable for comparing performance to standards depends on a variety of factors

- Annual comparisons may be appropriate for longer-run and higher-level standards.

Examples of Qualitative Standards:

(a) Improving the motivation level of employees.

(b) Improving labor relations.

(c) Improving the quality of products.

(d) Improving goodwill etc.

Thus, standards proceed as a lighthouse that warns and guides the ships at sea. Standards are the benchmarks towards which efforts of the whole organization are directed.

The procedure of controlling follows a sequence of reasonable steps as follows –

- Setting Standards

This is the first step of the control procedure. Before we start any other work, the managers need to set the standards against which the actual performances will be measured. These performance standards can be in the form of goals, such as revenue from sales over a period of time. Before these standards are set an appropriate study of the economy, situation and probability must be done so that the standards set are practical in nature. The standards should be attainable, measurable, and clear.

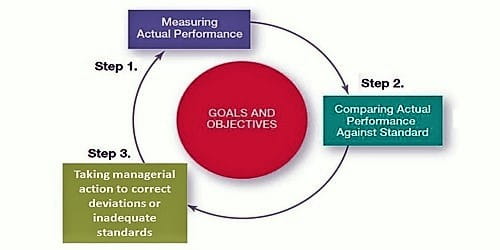

- Measurement of Actual Performance

The next consistent step in the control procedure is to measure the actual performance of the employees of the organization. The actual performance of the employee is measured against the target. However, this dimension of performances is not as straightforward as it sounds, particularly for non-technical jobs. When a manager is concerned with controlling sales, daily, weekly or monthly sales figures represent actual performance. With the increasing levels of management, the measurement of performance becomes difficult.

- Comparing Actual Performances with Standards

This comparison of the actual performances with the standards will make known the differences and deviations. This compares the degree of difference between the actual performance and the standard. In real case scenarios, these numbers almost never match up completely. It is completely necessary to evaluate deviations to determine why the standard is not being met when performance falls short of the standard. But managers need to ensure that these deviations are not beyond the acceptable ranges.

- Taking Corrective Action

It is initiated by the manager who corrects any defects in actual performance. This brings us to the final step of the control process. If the deviations in the third step are in an unacceptable range, then the firm needs to improve their performances. And the management must take action to get better the actual performance of the firm in those problem areas. After the reasons for deviations have been indomitable, managers can then build up solutions for issues with meeting the standards and make changes to processes or behaviors.