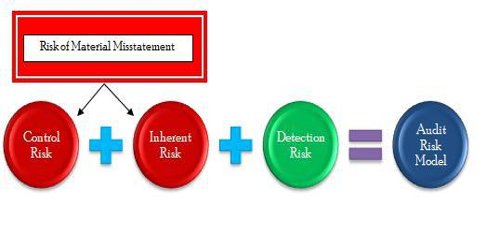

Audit Risk Model for Planning

Audit risk is the risk that the auditor may unknowingly fail to appropriately modify his or her opinion on financial statements that are materially misstated. It is the chance that financial statements will be issued with materials errors even though they have been reviewed by an auditor and approved.

The audit risk model is useful primarily for palming purpose is deciding how much evidence to accumulate in each year,

PDR = AAR / (IR x CR)

Planned deduction risk (PDR):

PDR is a measure of the risk that the auditor is willing to take that audit evidence for a segment will fail to detection errors exceeding a tolerable amount should such error exist.

There 2 key palms at planned deduction risk- It is dependent on other 3 factors in the model. DDR change only it the auditor changes one of the other factors.

It determines the amount of substantive evidence, the auditor pay to accumulate, inversely with the size of PDR reduced, the auditor needs to accumulate more evidence to achieve the reduced planned risk.

Acceptable (desired) audit risk (AAR): AAR is a measure o how willing the auditor is to accept that the financial statement may be materially misstated after the audit is completed and an unqualified opinion has been issued.

When the auditor decides on a lower AAR, it means the auditor wants to be more certain, that the financial statement is not materiality misstated, zero (0) risk would be complete uncertainty complete (0 Risk) of the accuracy financial statement is not economically practical.

Inherent Risk (IR): It is a measure of the auditor’s assessment of the likelihood that there are material errors in a segment before considering the effectiveness of the ICS.

Control Risk (CR): Control Risk is a measure of the auditor’s assessment of the likelihood that misstatements exceeding a tolerable amount in a segment will not be presented by the client’s internal controls.

Detection Risk (DR) – Detection risk is the risk that the auditor will not detect a material misstatement exists in an assertion.