Advantages and Disadvantages of Preference Shares

The Advantages of preference shares are given as follows:

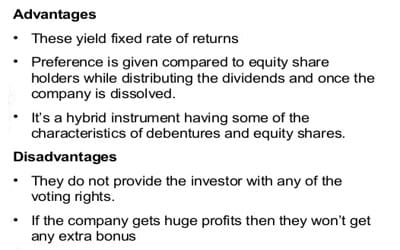

- Preference shares provide a reasonably steady income in the form of a fixed rate of return and safety of the investment. The company can thus maximize the profits that are accessible on the part of preference shareholders.

- Preference shares are useful for those investors who want the fixed rate of return with comparatively low risk. The possibility of a company’s capital market is widened as a consequence of the issuance of preference shares because of the reason that preference shares provide not only a fixed rate of return but also security to the investors.

- It does not affect the control of equity shareholders over the management as preference shareholders don’t have voting rights. There is thus no interference in general by the preference shareholders, even though they gain more profits and advantages over the general shareholders.

- Payment of a fixed rate of dividend to preference shares may enable a company to declare higher rates of dividend for the equity shareholders in good times. The dividends to be paid to the preference shareholders are fixed as compared to the equity shareholders.

- Preference shareholders have a preferential right of repayment over equity shareholders in the event of liquidation of a company. As a result of the issuance of preference shares, because dividends are paid only in the presence of profits; the absence of profits means absence of dividends.

- Preference capital does not create any sort of charge against the assets of a company. Because preference shares have no payment of dividends, no charges are levied on the assets of the company unlike in the case of debentures.

- By means of issuing exchangeable preference shares, flexibility in the company’s capital structure can be maintained because exchangeable preference shares can be redeemed under the terms of matter.

Disadvantages

The major limitations of preference shares as the source of business finance are as follows:

- Preference shares usually do not carry voting rights. As a result, preference shareholders are powerless and have no say in the management and control of the company.

- Preference shares are not suitable for those investors who are willing to take the risk and are interested in higher returns. In the case of preference shares, the credit value of a company is absolutely condensed because preference shareholders possess the right over the personal assets of the company.

- Preference capital dilutes the claims of equity shareholders over assets of the company. Because of the very basis that preference shareholders have preferential rights over the company assets in case of winding up of the company, dilution of equity shareholders claim over the assets take place.

- The rate of dividend on preference shares is generally higher than the rate of interest on debentures. The Company has to pay higher rates of dividends to the preference shareholders as compared to the regular shareholders. Thus the cost of capital of the company is also increased.

- As the dividend on these shares is to be paid only when the company earns the profit, there is no assured return for the investors. In order to attract sufficient investors, a company may have to offer a higher rate of dividend on preference shares. Thus, these shares may not be very attractive to investors.

- The dividend paid is not deductible from profits as the expense. Thus, there is no tax saving as in the case of interest on loans. In the case of preference shareholders, the taxable income of the company is not reduced while in the case of common shareholders, the taxable income of the company is reduced.