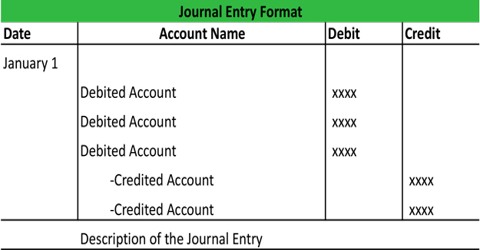

Steps in Journalizing

The procedure of analyzing the business transactions under the heads of debit and credit and recording them in the Journal is called Journalizing. An entry made in the journal is called a ‘Journal Entry’. The following steps are to be measured although journalizing entries for business transactions:

Step 1: Determine the two accounts which are concerned in the transaction. Evaluate the transaction and categorize the two accounts (single entry and compound entry) that are being affected by the transaction.

Step 2: Classify the above two accounts under Personal, Real or Nominal. Then determine the character of the accounts involved as real, personal or nominal.

Step 3: Find out the regulations of debit and credit for the above two accounts. Then verify which imperative of debit and credit is appropriate for each of the accounts involved.

As per the character and types of accounts, apply the rules of the journalization to give debit or credit effects.

Step 4: Identify which account is to be debited and which account is to be credited. Then determine the account to be debited and the account to be credited. Journal entries can be single entry i.e. one debit and one credit or can be multiple entries (one or more debits and one or more credits)

Step 5: Record the date of the transaction in the date column. The year and month are written once, till they change. The sequence of the dates and months should be strictly maintained.

Step 6: Enter the name of the account to be debited in the particulars column very close to the left-hand side of the particulars column followed by the abbreviation Dr. in the same line. Against this, the amount to be debited is written in the debit amount column in the same line.

Step 7: Write the name of the account to be credited in the second line starts with the word ‘To’ a few spaces away from the margin in the particulars column. Against this, the amount to be credited is written in the credit amount column in the same line.

Step 8: Write the narration within brackets in the next line in the specifics column. A transaction not including any person’s name is measured as a cash transaction. So, if a person’s name is given along with convincing words like ‘Cash’, ‘Bank’, ‘Received’, ‘Earned’, ‘Paid’, ‘Spent’, ‘Deposited’, ‘Withdrawn’, ‘Borrowed’, etc. then the transaction is measured as “Cash Transaction”.

Step 9: Draw a line across the entire specifics column to divide one journal entry from the other. In the particulars column, account to be debited on the first line with the abbreviation ‘Dr.’ on the right side of the similar line.

Conclusion:

First of all, read and identify with the transaction because it might be either in a cash transaction or credit transaction. In a credit transaction, out of the two accounts in the transaction, definitely, one account is Personal Account and the second account is Real Account. Record the date of the transaction in the first column which is the date column.