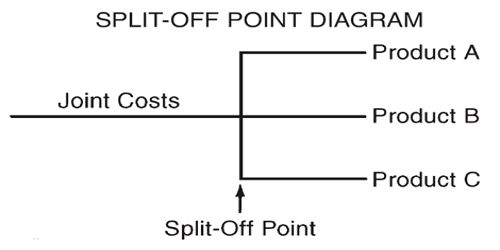

Split-off-point: The split-off point is the point in a production process where jointly manufactured products are henceforth manufactured separately; thus, their costs can be identified individually after the split-off point. A split-off point is a location in a production process where jointly manufactured products are henceforth manufactured separately; thus, their costs can be identified individually after the split-off point. The juncture in a production process where the product stream splits into two or more distinct products which become identifiable as joint products. Prior to the split-off point, production costs are allocated to jointly manufactured products. It is the moment inventory becomes an actual cost of the company’s financial statement.

Example: When sawing timber, both lumber and scrap wood appear, thus the activity of sawing is the split-off point in this production process.