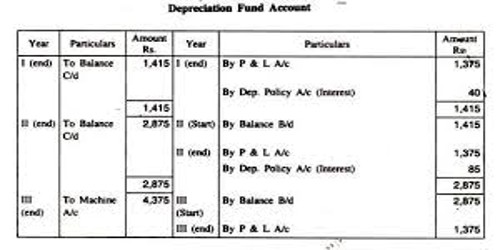

Depreciation Fund Method or Sinking Fund Method for Calculating Depreciation

Under this method, funds are made available for the replacement of asset at the end of its useful life. The depreciation remains the same year after year and is charged to Profit and Loss account every year through the creation of depreciation fund. The sinking fund method of depreciation is used when an organization wants to set aside a sufficient amount of cash to pay for a replacement asset when the current asset reaches the end of its useful life.

The amount of annual depreciation is invested in good securities bearing interest at a specified rate. The aggregate amount of interest and annual provision is invested every year. When the asset is completely written off or is to be replaced, the securities are sold and the amount so realised by selling securities is used to replace the old asset.

Merits (Depreciation Fund):

- This method provides liquid funds at the end of economic life of the existing asset to replace it with a new asset.

- This method is valuable for wasting assets.

- The amount of depreciation, charged to Profit and Loss Account, is invested in outside securities in order to earn compound interest. Thus, the system is beneficial to the business.

Demerits:

- This method is complicated and involves numerous calculations.

- Marketable securities always have some kind of uncertainty in terms of price fluctuations.

- Profit and Loss Account is burdened heavily by fixed amount of depreciation together with the cost of increasing repairs every year.

- This system works on the basis of original historical cost. The price changes are not considered.