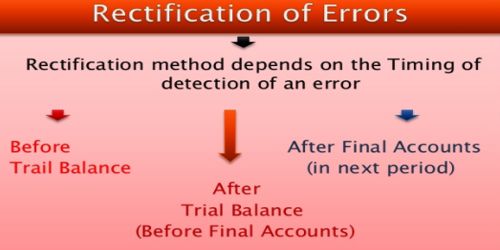

Rectification of Errors

Correction of errors in the books of financial records is not finished by erasing, rewriting or striking the figures which are incorrect. Correcting the errors that has occurred is called Rectification. Proper entry is conceded or appropriate descriptive note is written in the exacting account or accounts to neutralize the consequence of errors.

From the point of rectification, errors may be classified as follows:

- Single sided errors are errors which affect one side of an account.

- Double sided errors are errors which affect both the accounts in a transaction.

Explanation Error which do not affect the trial balance or two side errors

When an account has wrongly been debited in place of another accounts.

Example:

Machinery purchased for Rs 100000 has been debited to Purchase A/c

Method of rectification:

Solution:

Correct entry:

Machinery A/c dr 100000

To cash A/c 100000 (being machinery purchased)

Wrong entry:

Purchased A/c Dr 100000

To cash A/c 100000 (being goods purchased)

Compare:

Now compare wrong entry with correct entry and make rectifying entry in this case we have to Debit Machinery a/c but we did not do that and debit wrong a/c purchase now To rectify we have to debit Machinery a/c and to cancel purchase we have to credit purchase.

Therefore rectifying entry will be:

Machinery A/c Dr 100000

To Purchase A/c 100000 (being rectification entry)