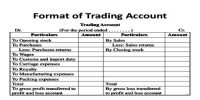

Profit and Loss Account

After calculating the gross profit or gross loss the next step is to prepare the profit and loss account. To earn net profit a trader has to acquire many expenses apart from those spent for purchases and manufacturing of goods. If such expenses are less than gross profit, the result will be net profit. When total of all these expenses are more than gross profit the result will be net loss. Profit and loss accounts show your total income and expenses, and also shows whether your business has earned more income than it has spent on its running costs. If that is the case, then your business has made a profit. This account shows what net profit or loss your business has made within an accounting period after deducting all expenditure from income. A net profit is earned if total expenditure is less than the sales and a net loss if it is greater.

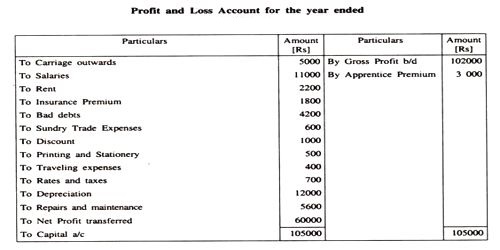

The particulars required for the preparation of profit and loss account are available from the trial balance. Only indirect expenses and indirect revenues are considered in it. This account starts from the result of trading account (gross profit or gross loss). Gross profit is shown on the credit side of the profit and loss account and gross loss is shown on the debit side of this account. All indirect expenses are transferred on the debit side of this account and all indirect revenues on credit side.

Need: The aim of profit and loss account is to ascertain the net profit earned or net loss suffered during a particular period. The Profit and Loss Account statement is also referred to as “statement of profit and loss”, “income statement,” “statement of operations,” “statement of financial results,” and “income and expense statement.”