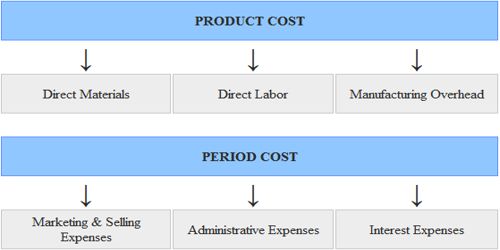

Product versus Period Cost

A manufacturer’s production costs are the direct materials, direct labor, and manufacturing overhead used in making its products. (Manufacturing overhead is also referred to as factory overhead, indirect manufacturing costs, and burden.) The product costs of direct materials, direct labor, and manufacturing overhead are also “inventoriable” costs since these are the necessary costs of manufacturing the products.

Costs that become part of the cost of goods manufactured are called product costs. Such costs are incurred on the manufacturing process either directly as material and labor costs or indirectly as overheads. Period costs are basically all costs other than product costs. These are not incurred during the manufacturing process and therefore these cannot be assigned to cost goods manufactured. Period costs are not a necessary part of the manufacturing process. As a result, period costs cannot be assigned to the products or to the cost of inventory. The period costs are usually associated with the selling function of the business or its general administration. The period costs are reported as expenses in the accounting period in which they (1) best match with revenues, (2) when they expire, or (3) in the current accounting period. In addition to the selling and general administrative expenses, most interest expense is a period expense.

Inventoriable costs are (1) the costs to purchase or manufacture products which will be resold, plus (2) the costs to get those products in place and ready for sale. Inventoriable costs are also known as product costs.

To illustrate, let’s assume that a retailer purchases an item for resale by paying $20 to the supplier. The item is purchased FOB shipping point, which means that the retailer must pay the height from the supplier to its location. If that freight cost is $1, then the retailer’s inventoriable cost is $21. Assuming this is the only item in the retailer’s inventory, the retailer’s balance sheet will report inventory at a cost of $21. When the item is sold, the retailer’s inventory will decrease by $21 and the $21 will be reported on the income statement as the cost of goods sold.

In the case of a manufacturer, a product’s inventoriable costs are the costs of the direct materials, direct labor, and manufacturing overhead incurred in manufacturing the product.