Items which are included in the debit side of the trading account

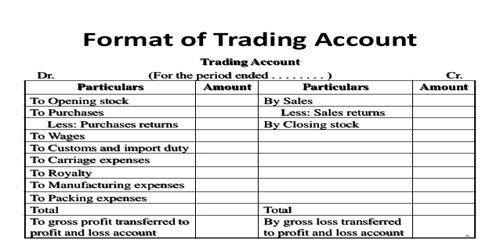

Trading means buying and selling. The trading account demonstrates the effect of buying and selling of goods. The primary step of the final account is a trading account. It is a nominal account which is prepared at the end of the accounting year. The trading account helps to find out gross earnings or gross loss during the accounting period.

Opening stock consists of raw materials, work in progress, and finished goods depending upon the nature of business. In the merchandising business, the opening stock consists of finished goods. In a manufacturing concern, opening stock consists of raw materials.

Purchase

Purchase includes both credit purchase and cash purchase. Purchase is available in the trial balance. Traders generally purchase goods on cash or on credit. The purchases are debited to the Trading Account after deducting Purchase Returns if any. The deductions are shown in the inner column and net purchases are shown in the outer column.

Purchase Returns

Purchase returns appear on the credit side of the trial balance. Purchase returns may be shown by deduction from purchases. Thus the Net Purchases are debited to Trading Account and Closing Stock is shown in the Balance Sheet.

Direct Expenses

Direct expenses are those expenses that have been incurred to bring the goods or making the goods ready for sale. All such expenses are debited to Trading Account. Direct expenses mean all the expenses which are directly attributable to the purchase of goods. These are some examples of direct expenses.

- Manufacturing expenses.

- Commission on purchase – Workers may be employed to manufacture merchandise or make it more saleable. Similar types of items are debited to Trading Account.

- Direct labor or direct wages – Wages paid to workers, who are directly engaged in the production, are direct expenses.

- Freight on purchase – These items fall under direct expenses. These are transportation expenses met for bringing the goods purchased to the business place.

- Import Duty/Customs Duty: In the case of goods imported from abroad, import duty, customs duty or dock charges, etc. have to paid. Since these are related to the purchase of goods for resale purposes, these expenses are shown in the debit side of the Trading Account.

- Fuel, power, and lighting expenses – Machines are used in the production process with the help of coal or electricity. Such charges are direct and are debited to Trading Account.

- Packing charges – Sometimes, it is necessary to pack the goods in a special type of packages in order to protect the goods or attract the customers. In these circumstances, the cost of packaging is a direct expense and is debited to Trading Account.