Along with direct labor charges, there are other costs linked to direct labor personnel. These are idle time, overtime premium along with fringe benefits which can be provided to personnel. These are not a part of direct labor expenses. The following paragraphs explain the working out and accounting treatment of idle occasion, overtime premium along with labor fringe rewards:

Treatment of idle time:

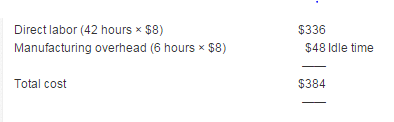

Idle time is the unproductive time of employees for which they are still paid. Idle time means the volume of time the personnel remains idle in a normal working morning. The idle occasion is usually caused by a sudden fault in machine or tools, power failure, deficiency of orders for the merchandise, inefficient work booking, defective materials along with a shortage of raw materials, etc. The cost linked to idle time is usually treated as oblique labor cost and really should, therefore, be incorporated into manufacturing overhead expenses. For example, the normal weekly working hours of the worker are 48 and they are paid @ $8 each hour. If he is still idle for 6 hours due to power failure, then the cost of 42 hours could well be treated as one on one labor cost and the cost of 6 hours (idle time) could well be treated as oblique labor cost and incorporated into manufacturing overhead expense.

The cost associated with idle time is treated as indirect labor cost and should, therefore, be included in manufacturing overhead cost. In cost accounting, the cost of such idle time is included as either direct labor or manufacturing overhead and is part of the total product cost.

Treatment of overtime premium:

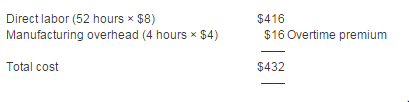

Overtime premium could be the amount that can be paid, for this overtime worked, well over the normal income rate. Like lazy time, overtime premium is also treated as oblique labor cost and included in manufacturing overhead charges. For example, a worker typically works for 48 hours every week @ $8 by the hour. In a specific week, if he works for 52 several hours and company pays off him $12 for each and every hour worked well over 48 hours, the allocation in the labor cost in the worker would be generated as follows:

The amount of $16 is overtime premium and is a part of manufacturing overhead cost. Like idle time, overtime premium is also treated as indirect labor cost and included in manufacturing overhead cost. Employees who work night shifts or other anti-social hours may be entitled to a shift allowance or shift premium.

Treatment of labor fringe benefits:

Fringe benefits are benefits that recruiters provide to employees as well as normal salaries or even wages. Examples connected with fringe benefits are hospitalization, insurance plans, retirement plans, paid holidays and investment, etc. Most with the companies treat toil fringe benefits since indirect labor along with, therefore, include all of them in manufacturing expense costs. Fringe benefits are a form of pay, often from employers to employees, and considered compensation for services beyond the employee’s normal rate of pay.

A few firms treat direct labor related fringe rewards as addition immediate labor cost that’s considered a more superior practice. Most of the companies treat labor fringe benefits as indirect labor and, therefore, include them in manufacturing overhead costs.

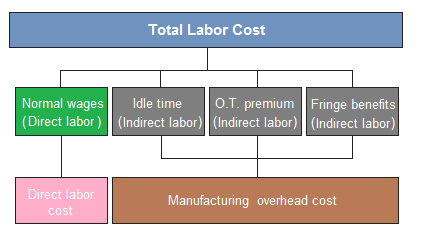

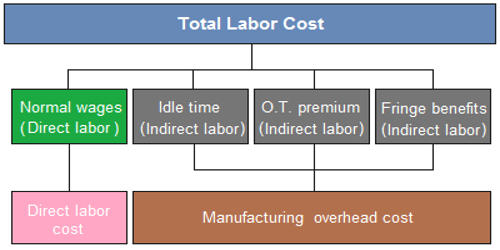

The above information has also been summarized below: