Trading means buying and selling. The trading account demonstrates the effect of buying and selling of goods. The primary step of final account is a trading account. It is a nominal account which is prepared at the end of the accounting year. Trading account is a report or statement which is prepared by a business firm. It shows the gross profit of business actions during a particular period.

A trading account helps to find out gross earnings or gross loss during the accounting time. It is the first step in the procedure of preparing the final accounts of a company. It is calculated by comparing the net sale with the cost of goods sold (COGS).

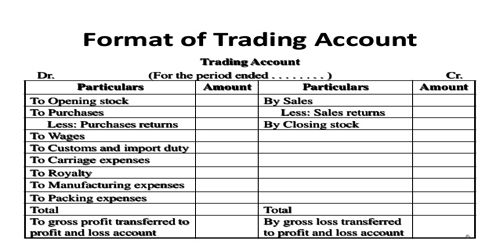

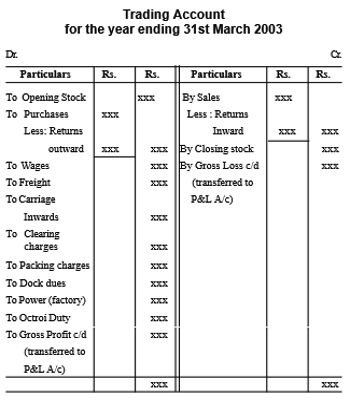

The format of Trading Account –

Items appearing in the debit side

(1) Opening stock: Stock on hand at the opening of the year is termed as opening stock. The closing stock of the earlier accounting year is brought forward as opening stock of the present accounting year. In the case of a new business, there will not be any opening stock. It consists of raw material, work in progress, and finished goods.

(2) Purchases: Purchases made during the year, includes both cash and credit purchases of goods. Purchase returns must be deducted from the total purchases to get net purchases. The goods may have been acquired in cash or credit and once purchased if the goods are returned to the supplier for any reason it becomes a part of purchase returns or returns outward.

(3) Direct Expenses: Expenses which are incurred from the stage of purchase to the stage of making the goods in saleable condition are termed as direct expenses. All direct expenses like Carriage inward & Freight Expenses, Rent for factory, Electricity and Power expenses, wages of workers and supervisors, Packing expenses, etc.

Some of the direct expenses are:

- Wages: It means remuneration paid to workers.

- Carriage or carriage inwards: It means the transportation charges paid to bring the goods from the place of purchase to the place of business.

- Customs duty, dock dues, clearing charges, import duty, etc. These expenses are paid to the Government on the goods imported.

- Other expenses: Fuel, power, lighting charges, oil, grease, waste related to production and packing expenses.

Items appearing in the credit side

(i) Sales: Goods sold in cash and credit by the business to earn profits are included under the head “Sales”. This includes both cash and credit sale made during the year. Net sales are derived by deducting sales return from the total sales. Items once sold may be returned by the customers due to various reasons which are termed as sales returns or returns inward.

(ii) Closing stock: The unsold stock in hand at the end of the current accounting period is placed under the head “closing stock”. The Closing stock is the worth of goods which remain in the hands of the trader at the end of the year. It does not appear in the trial balance. It appears outside the trial balance. (As it appears outside the trial balance, first it will be recorded in the credit side of the trading account and then exposed in the assets side of the balance sheet). It is valued at the end of an accounting period at cost or net realizable value whichever is lower.

With the help of a trading account, Sales Tax Authorities can simply observe the correct purchases and correct sales as per the sales tax return submitted by a business firm. The management decides the price of the product with the help of a trading account, after keeping in mind the market competition.