Purchase book is an exceptional function secondary book organized by a business to record all credit purchases. It is a particular journal used by businesses to record all credit purchases. It does not hold the record of Purchases of assets.

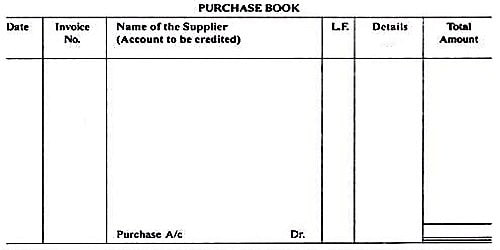

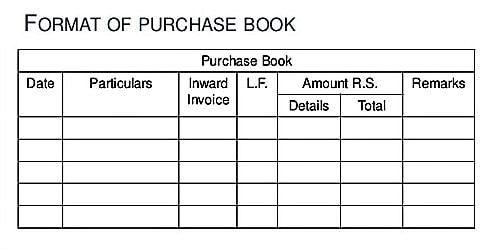

Format of Purchase Book –

Explanations to Various Columns of Purchase Book:

- Date Column

It represents the date on which the deal took place. The date column is used to record the date on which the invoice belonging to goods purchased is received. In this column, the date of the transaction, on which goods were purchased on credit, shall be recorded. The date column is used to record the date of purchase of merchandise.

- Invoice Number or date column

The invoice date column is used to record the date on which the invoice is organized by the supplier. The number of invoice (i.e., basis document) showing the purchase of goods shall be recorded in this column. Amount column is used to record the amount of invoice. Invoice number column is used to record the invoice number for reference. The amount payable on the invoice is recorded in this column.

- Name of the Suppliers

The supplier’s name is written in this column. Some businesses also contain a short description of goods purchased in this column. In this column, name of the individual/supplier, from whom the goods were purchased, shall be written along with the detailed narrative of goods viz., amount, quality, rate, gross amount, trade discount and sales tax, etc.

- Ledger Folio (L.F.)

This column shows the page number of the suppliers account in the ledger accounts. The page number of the ledger of the supplier on which the transaction is recorded shall be recorded in this column.

- Payment terms column

This column is used to record the payment terms allowed by the supplier. Accounts credited column is used to record the name of business concern from whom merchandise is purchased on account.

- Details

It reveals the number of goods purchased and the amount of trade discount. The individual total amount of various items, if purchased from the same supplier, shall be recorded in this column. Total trade discount by the supplier and sales tax paid (if any) shall also be adjusted in this column.

- Reference column

At the finish of each day, the entries from purchases journal are posted to individual accounts in the accounts payable supplementary ledger. Posting reference column is used to write the account number while posting into the ledger. It indicates that posting has been made. If computer software is used, these entries are instantly posted to the subsidiary ledger. Reference column is used to record the account numbers of the accounts to which the entries have been transferred. If accounts are not numbered, the page number of accounts is recorded in this column.

- Total Amount

This column represents the net price of the goods, i.e, the amount which is payable to the creditors after adjusting discount and expenses if any. The total of this column shall be transferred to the debit side of the purchases account.

- Items columns

These columns are used to enter the cost of individual items purchased from suppliers such as inventory, store supplies, office supplies, and equipment, etc. The number of item columns to be used on a purchases journal depends on the nature and requirement of each individual business.

At the end of each month, the purchase book is totaled. Information such as the description of goods or services received, the number of goods purchased and credit terms are usually on the face of invoice but may be recorded in purchases journal as well. The total shows the total amount of goods or materials purchased on credit.