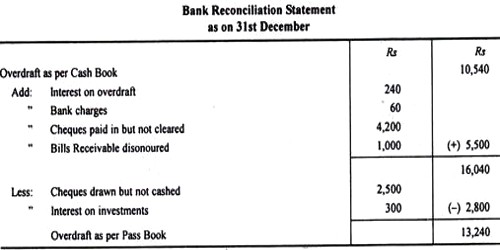

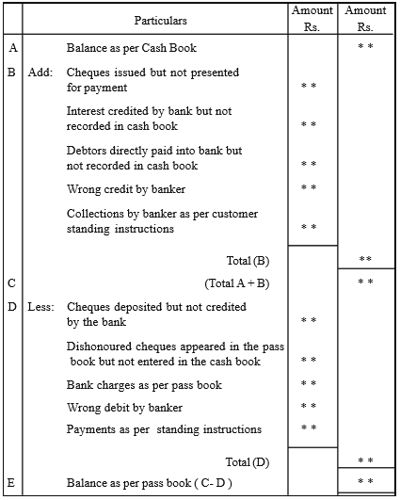

The format of Bank Reconciliation Statement

‘Bank reconciliation statement is a catalog in which a variety of substance that reason a dissimilarity between bank balance as per cash book and pass book on any given date are indicated’. The format of Bank Reconciliation Statement when bank balance as per cash book is taken as the starting point.

Bank Reconciliation Statement as on …

Points to be noted:

To work out the problems on Bank Reconciliation Statement, the following points are to be remembered.

(i) The heading is given as “Bank Reconciliation Statement as on ____________”

(ii) All items to be added are grouped together and shown in the inner column and the total is taken to the outer column for the purpose of addition (B ).

(iii) All items to be deducted are grouped together in the inner column and the total can be shown in the outer column for deduction.(D).

(iv) Favourable balance means the cash book will have a debit balance and the passbook will have a credit balance.

(v) Bank overdraft or unfavourable balance means cash book will have a credit balance and passbook will have debit balance.

Following are the transactions which typically come into view in bank statement but not in company’s cash account:

- Service Charges: Service charges might have been deducted by the bank. Such charges are usually not known to the company before the issuance of bank statement.

- Interest Income: If any interest income has been earned by the company on its bank account, it is not generally entered in company’s cash account before the issuance of bank statement.