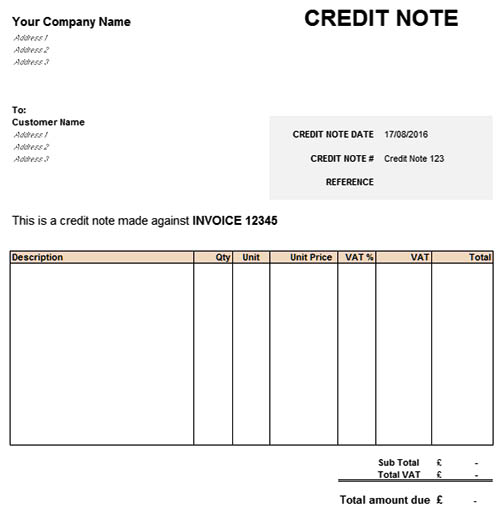

Credit Note is a tool used to notify that the other party’s account is credited in his books. It encloses the date on which goods are returned, the name of the client, details of the goods received back, the number of such goods and reasons for returning the goods. Debit Note is issued by the buyer, at the time of returning the goods to the vendor, and the vendor issues a Credit Note to notify that he/she has received the returned goods. Each credit note is in sequence number. A replica copy of the credit note is retained for the record function. On the source of a credit note, the customer’s account is credited in the books.

A credit note is a paper sent by a seller to its buyer or, in other words, a vendor to the purchaser, notifying that a credit has been provided to their account against the goods returned by the purchaser. It includes details such as the credit amount, date of issue and the cause for issuing the credit. It is also known as a credit memo, which is short for “credit memorandum.” It reduces the amount due to be paid by the purchaser, and then it allows additional purchases in lieu of the credit note itself. This is a commercial document that the supplier produces for the purchaser to notify the customer that credit is being functional to the customer for different reasons.

Credit notes are issued when there is a descending revision in prices of goods or services supplied. It can be compared to a negative invoice that has the ability to invalidate the effects of an invoice. It offers a decrease in the value of the invoice and thus, reduces the accountability of the buyer. It is often inflicted with a return of goods to the supplier. It always has a negative impact on the accounting balance in the books of the seller.

Few Characteristics of a Credit Note

- A credit note is sent to inform about the credit made in the account of the buyer along with the reasons mentioned in it.

- The sales return book is updated on the basis of the credit note. (In case of return of goods) The sales return book is updated on its basis.

- It is issued when a customer returns the goofs and the value of similar may be less or equal to the amount he had already paid.

- It is generally sent by the seller if the goods are found unfinished, damaged or inaccurate at the buyer’s end.

- The entry is made in sales work in the case where goods are returned.

- A credit note usually shows a negative amount.

A credit note is issued for the cost of goods returned by the consumer, it might be less than or equivalent to a total amount of the order. This note is efficiently a negative invoice – it’s a method of showing a purchaser that they don’t have to reimburse the full amount of an invoice. This note might either cancel an invoice out totally if it’s for a similar amount as the invoice, or it might be for less than the invoice. Therefore, the seller may propose several gift or store credit to the buyer.