EconomicsThe concept of consumer surplus Consumer surplus is defined as the difference between the consumers’ willingness to pay for a commodity and the actual price paid by them or the…

EconomicsConsumer’s surplus by using indifference curve Consumer’s Surplus is one of the most important concepts in Economics. It was expounded by Alfred Marshall. It needs careful study. In our daily expenditure,…

EconomicsEngle Curve The Engle Curve tracks the consumption of a Good X as an individual’s income changes. Income is plotted on the x-axis and the quantity of Good X…

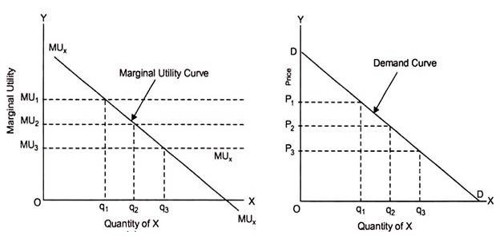

EconomicsUtility and Marginal Utility The problem of fulfilling the unlimited wants of humankind with limited or scarce resources. Because of scarcity, economies need to allocate their resources efficiently. Underlying the…

EconomicsOpportunity cost Scarcity of resources is one of the more basic concepts of economics. Scarcity necessitates trade-offs, and trade-offs result in an opportunity cost. While the cost…

EconomicsWhat is indifference curve? When a consumer consumes various goods and services, then there are some combinations, which give him exactly the same total satisfaction. The graphical representation of…

EconomicsU-shaped cost curves The U-shapes of the average total cost, average variable cost, and marginal cost curves are directly or indirectly the result of increasing marginal returns for…

EconomicsDifference between Marginal cost and Average Cost Difference between Marginal cost and Average Cost: Marginal Cost Marginal cost is the change in total cost when an additional unit of output is produced.…

EconomicsProduction Possibility Frontier Production Possibility Frontier shows the maximum amounts of production that can be obtained by an economy given its technological knowledge and quantity of imputes available. Opportunity…

EconomicsBasic Assumption of Marshallian Utility Analysis The cardinal utility approach or what is called also as the Marshallian approach to consumer’s equilibrium is based on the following assumption – Rationality It…