In secularization, certain assets that have a cash flow are pooled and bonds (or short-term commercial paper) are issued to fund these assets. Highly rated bonds, called senior bonds, are issued up to a certain proportion of the assets pooled (usually 90%), and subordinated bonds for the rest (the balance of usually 10%). The split depends on the rating agencies’ credit-enhancement demands.

The subordinated bonds are further split into so-called mezzanine bonds (to the extent of about 7%) and junior bonds for the balance (about 3%). The mezzanine bonds are usually rated BBB and the junior bonds are unrated (because they are usually taken up by the sponsor of the secularization).

In the event of the failure of a portion of the underlying assets, the holders of the junior bonds are the first to take the loss. Next in line are the holders of the mezzanine bonds and last in line are the holders of the highly rated senior bonds. Thus the junior bonds are subordinated to the mezzanine bonds and the mezzanine bonds are subordinated to the highly rated senior bonds.

These bonds are usually of the plain vanilla variety, but some are floating rate bonds.

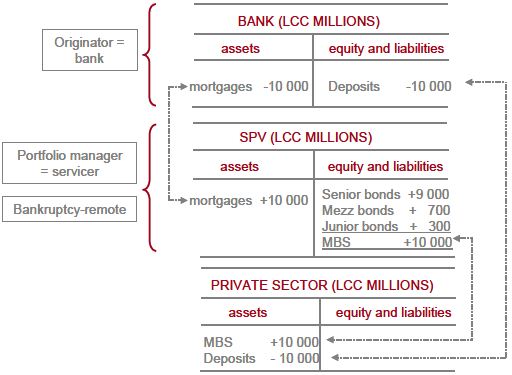

An example of a secularization of mortgages by a bank is presented in Figure, for the sake of didactic elucidation. In this example it is assumed that all the mortgage backed securities (MBS) have been purchased by members of the financial private sector (pension funds, insurers and so on). In reality the junior (unrated) bonds are taken up by the originator / sponsor (usually a bank), while the mezzanine bonds are taken up by some risk-taker because the rate offered on them is high, reflecting the risk profile of these bonds.