Ways of narrowing Expectation Gap:

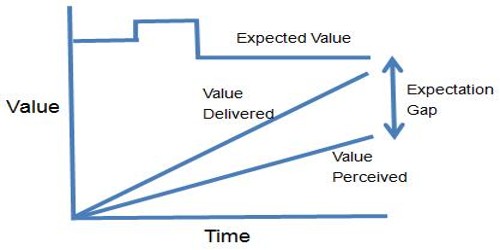

The term expectation gap is defined as a gap between the expectation of users of assurance reports, particularly of audit report under the companies act and the firm’s legal responsibilities. It is the gap between an auditor’s actual standard of performance and the more rigorous public expectation of what an auditors performance should be.

Expanding the audit report: The content of audit report should be expanded to:

(a) Set out the responsibilities of both the auditors and the directors.

(b) Explain how an audit is conducted:

- On a test basis which implies sampling

- By assessing significant estimates and judgments

- So as to give reasonable assurance on the financial statements.

- So as to detect material misstatements in relation to frauds and errors or another irregularity.

Engagement letter: The auditor should issue an engagement letter including a paragraph regarding the responsibilities of directors as well as the responsibilities of the auditors.

Director’s responsibilities: In the audit opinion the auditor should mention the responsibilities of directors as well as the responsibilities of the auditors.

Audit committee: The auditor should inform the audit committee regarding any fraud of error or any irregularities on a timely basis.