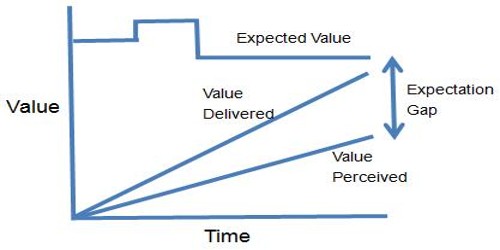

Reasons for raising Expectation Gap

The term expectation gap is defined as a gap between the expectation of users of assurance reports, particularly of audit report under the companies act and the firm’s legal responsibilities. It is the gap between an auditor’s actual standard of performance and the more rigorous public expectation of what an auditors performance should be.

Reasons for raising expectation gap-

(a) Preparation of financial statement: Many users believe that responsibility for preparing financial statement lies with the auditors rather than with management.

(b) Detection of frauds: It is widely believed by the general public that the auditor’s principal duty is to detect frauds, when in fact the duty is to make a report as to whether or not the financial; statements are materially misstated irrespective of whether such misstatement arises as a result of frauds.

(c) The concept of materiality: In most the users of the financial statement will also have little perception of the concept of materiality and believe that the auditors check all the transactions that the company undertakes.

(d) Perception: The public generally perceives that an audit report attached to the financial statements means that they are correct rather than just meaning that there is reasonable assurance that they give a true and fair view.