Investment Decision in Financial management

An investment decision revolves around spending capital on assets that will yield the highest return for the company over a desired time period. A firm’s resources are scarce in comparison to the uses to which they can be put. A firm, therefore, has to choose where to invest these resources, so that they are able to earn the highest possible return for their investors. The investment decision, therefore, relates to how the firm’s funds are invested in different assets.

Generally, investment decisions fall under two broad categories:

(i) Investment in own business; and

(ii) Investment in outside business, i.e., in securities and other companies.

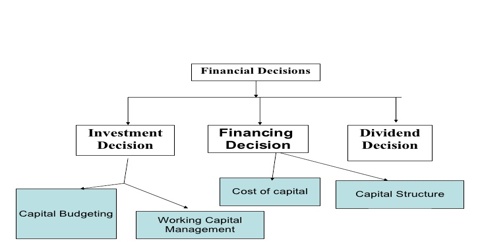

Investment decision can be long-term or short-term. A long-term investment decision is also called a Capital Budgeting decision. It involves committing the finance on a long-term basis. For example, making investment in a new machine to replace an existing one or acquiring a new fixed asset or opening a new branch etc. These decisions are very crucial for any business since they affect its earning capacity over the long run. The size of assets, the profitability and competitiveness are all affected by the capital budgeting decisions. Moreover, these decisions normally involve huge amounts of investment and are irreversible except at a huge cost.

A bad capital budgeting decision normally has the capacity to severely damage the financial fortune of a business. Short term investment decisions (also called working capital decisions) are concerned with the decisions about the levels of cash, inventories and debtors. These decisions affect the day to day working of a business. These affect the liquidity as well as profitability of a business. Efficient cash management, inventory management and receivables management are essential ingredients of sound working capital management.