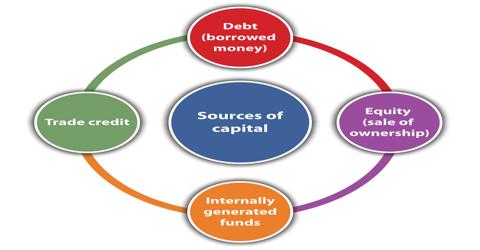

Factors that Affecting Source of Funds

The choice of the source of finance depends upon a number of factors further depending upon the time, purpose, type of organization, etc. Financial needs of a business are of different types — long term, short term, fixed and fluctuating. Therefore, business firms resort to different types of sources for raising funds. Short-term borrowings offer the benefit of reduced cost due to the reduction of idle capital, but long – term borrowings are considered a necessity on many grounds. Similarly equity capital has a role to play in the scheme for raising funds in the corporate sector.

The factors that affect the choice of source of finance are briefly discussed below:

(i) Cost:

There are two types of cost viz., the cost of procurement of funds and the cost of utilizing the funds. Both these costs should be taken into account while deciding about the source of funds that will be used by an organization.

(ii) Financial strength and stability of operations:

The financial strength of a business is also a key determinant. In the choice of source of funds, the business should be in a sound financial position so as to be able to repay the principal amount and interest on the borrowed amount.

(iii) Form of organization and legal status:

The form of business organization and status influences the choice of a source for raising money. Sole proprietorship and partnership firm can’t raise funds by the issue of shares or debentures, whereas Joint Stock Companies prefer issue shares and debentures to raise funds. A partnership firm, for example, cannot raise money by the issue of equity shares as these can be issued only by a joint-stock company.

(iv) Purpose and time period:

A business should plan according to the time period for which the funds are required. A short-term need, for example, can be met through borrowing funds at a low rate of interest through trade credit, commercial paper, etc. For long term finance, sources such as the issue of shares and debentures are more appropriate.

(v) Risk profile:

Businesses should evaluate each of the sources of finance in terms of the risk involved. Owners’ fund securities (equity, retained earnings) involve no risk whereas borrowed fund securities are risky securities. For example, there is the least risk in equity as the share capital has to be repaid only at the time of winding up and dividends need not be paid if no profits are available. Accordingly, the business should choose the source of finance.

(vi) Tax benefits:

Various sources may also be weighed in terms of their tax benefits. Interest on debentures, loans are deducted from the profits of the company before calculating corporation tax, whereas dividend paid to equity shareholders is not deducted from the total income. For example, while the dividend on preference shares is not tax-deductible, interest paid on debentures and loans is tax-deductible and may, therefore, be preferred by organizations seeking tax advantage.

(vii) Control:

A particular source of funds may affect the control and power of the owners on the management of a firm. Voting rights of equity shareholders enable them to have control over the business, whereas borrowed capital securities do not dilute the control of management over the business. The issue of equity shares may mean the deletion of the control.