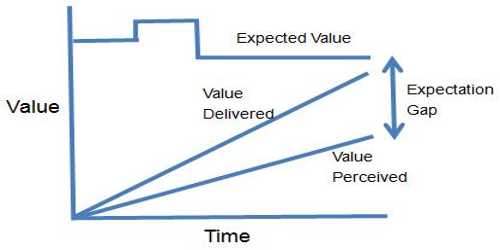

The term expectation gap is defined as a gap between the expectation of users of assurance reports, particularly of audit report under the companies act and the firm’s legal responsibilities. Expectation gap can also be explained as the difference between the effectiveness of audit engagement what users believe and what the auditor believes. Expectation gap is related to audit can also be explained as the difference between the expectation of user and auditor himself on the responsibilities of the auditor. It can also refer to the difference in understanding regarding the nature of audit engagement i.e. what users believe an audit is and what audit actually is.

In short, it is all about what auditor expects and what others expect from the auditor. For last few years this gap has been debated a number of times at different forums and stakeholders have agreed on reducing this gap as most of the time it has been bone of contention between client, auditor, and other users of financial statements.

How can this gap be narrowed down?

(a) Users must understand why the auditor can only provide reasonable assurance and not the absolute assurance and what inherent limitations of the audit are.

(b) Users must understand that general purpose financial statements are meant for general needs of users and even if they have been audited in the best way possible but it does not mean audited financial statements can help in any decision-making situation.

(c) Users must realize that auditor’s work is relative to circumstances that require the use of judgment which may be wrong. Although auditor works diligently it does not always mean if the judgment is wrong then auditor is guilty of ignorance rather it will be assessed based on what auditor could possibly do and what he actually did.

(d) Although auditor and management are required to produce financial statements in a way that are easy to understand users are also expected to have a certain degree of relevant knowledge on how to use and interpret financial statements. Financial statements are not for everyone to read and act upon.

(e) For auditors to understand users’ expectations they must arrange workshops or seminars so that users at least feel that they have been heard. An auditor must not rule out everything on the basis of lack of knowledge on part of users.

(f) An auditor must make audit reports easy to understand for the masses and avoid too great extent any technical jargon that can impair an ordinary person’s understanding that lack the skillful insight of financial statements.

(g) The auditor is already providing less than absolute assurance so he must not leave any effort undone to maintain a reasonable level of assurance by complying with the requirements of relevant auditing standards. For example, proper planning, an appropriate understanding of entity to design further audit procedures, maintaining sceptic attitude, reducing sampling risk to appropriate level etc.