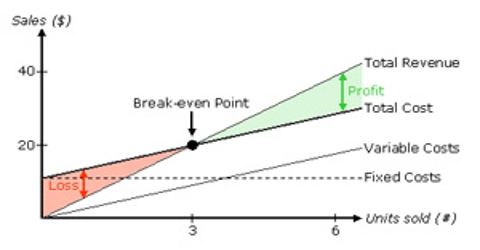

Breakeven analysis is a method used by managers to study the connection among costs, volume and profits. It determines the possible profit and losses at diverse levels of activity. The sales volume at which there is no profit, no loss is known as breakeven point. It is a helpful method for the managers as it helps in estimating profits at diverse levels of activities. Breakeven analysis is used to determine when your business will be able to cover all its expenses and begin to make a profit. It is important to identify your startup costs, which will help you determine your sales revenue needed to pay ongoing business expenses.

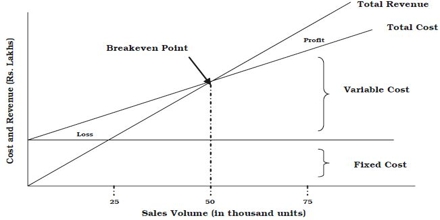

The figure shows breakeven chart of a firm. Breakeven point is determined by the intersection of Total Revenue and Total Cost curves.

The figure shows that the firm will break even at 50,000 units of output. At this point, there is no profit no loss. It is beyond this point that the firm will start earning profits. Breakeven point can be calculated with the help of the following formula:

Breakeven Point = [Fixed Costs / (Selling price per unit – Variable cost per unit)]

Breakeven analysis helps a firm in keeping a close check over its variable costs and determines the level of activity at which the firm can earn its target profit.