Working capital is money available to a company for day-to-day operations.

The formula for working capital is: Current Assets – Current Liabilities

How it works/Example:

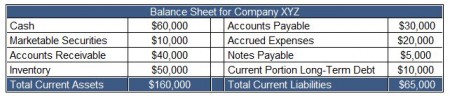

Here is some balance sheet information about XYZ Company:

Using the working capital formula and the information above from Figure 1, we can calculate that XYZ Company’s working capital is:

$160,000 – $65,000 = $95,000

Why it Matters:

Working capital is a common measure of a company’s liquidity, efficiency, and overall health. Because it includes cash, inventory, accounts receivable, accounts payable, the portion of debt due within one year, and other short-term accounts, a company’s working capital reflects the results of a host of company activities, including inventory management, debt management, revenue collection, and payments to suppliers.

Positive working capital generally indicates that a company is able to pay off its short-term liabilities almost immediately. Negative working capital generally indicates a company is unable to do so. This is why analysts are sensitive to decreases in working capital; they suggest a company is becoming overleveraged, is struggling to maintain or grow sales, is paying bills too quickly, or is collecting receivables too slowly. Increases in working capital, on the other hand, suggest the opposite. There are several ways to evaluate a company’s working capital further, including calculating the inventory-turnover ratio, the receivables ratio, days payable, the current ratio, and the quick ratio.

One of the most significant uses of working capital is inventory. The longer inventory sits on the shelf or in the warehouse, the longer the company’s working capital is tied up.

When not managed carefully, businesses can grow themselves out of cash by needing more working capital to fulfill expansion plans than they can generate in their current state. This usually occurs when a company has used cash to pay for everything, rather than seeking financing that would smooth out the payments and make cash available for other uses. As a result, working capital shortages cause many businesses to fail even though they may actually turn a profit. The most efficient companies invest wisely to avoid these situations.

Analysts commonly point out that the level and timing of a company’s cash flows are what really determine whether a company is able to pay its liabilities when due. The working-capital formula assumes that a company really would liquidate its current assets to pay current liabilities, which is not always realistic considering some cash is always needed to meet payroll obligations and maintain operations. Further, the working-capital formula assumes that accounts receivable are readily available for collection, which may not be the case for many companies.

It is also important to understand that the timing of asset purchases, payment and collection policies, the likelihood that a company will write off some past-due receivables, and even capital-raising efforts can generate different working capital needs for similar companies. Equally important is that working capital needs vary from industry to industry, especially considering how different industries depend on expensive equipment, use different revenue accounting methods, and approach other industry-specific matters. Finding ways to smooth out cash payments in order to keep working capital stable is particularly difficult for manufacturers and other companies that require a lot of up-front costs. For these reasons, comparison of working capital is generally most meaningful among companies within the same industry, and the definition of a “high” or “low” ratio should be made within this context.