The acid test ratio compares the most short-term assets to short-term liabilities. The intent of this ratio is to evaluate whether a business has sufficient cash to pay for its immediate obligations. If not, there is a significant risk of default. The formula is:

![]()

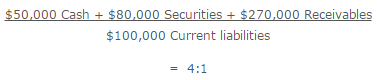

For example, a business has $50,000 of cash, $80,000 of marketable securities, and $270,000 of accounts receivable, which are offset by $100,000 of current liabilities. The calculation of its acid-test ratio is:

The ratio is most useful in those situations in which there are some assets that have uncertain liquidity, such as inventory. These items may not be convertible into cash for some time, and so should not be compared to current liabilities. Consequently, the ratio is commonly used to evaluate businesses in industries that use large amounts of inventory, such as the retail and manufacturing sectors.

Though generally reliable, the ratio can yield incorrect indications in the following situations:

- When a company has an unused line of credit. In this case, it may have little or no cash on hand, and yet can draw upon the cash in the line of credit to pay its bills.

- When current liabilities are delayed. By definition, current liabilities include any liabilities due within the next year. A liability due at the far end of this period still appears in the denominator, even though there is no immediate need to pay it.

Similar Terms

The acid test ratio is also known as the quick ratio and acid ratio.