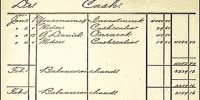

A subsidiary ledger is a group of accounts with a common characteristic.

Subsidiary ledgers are of various types, such as:

- Accounts receivable subsidiary ledger,

- Accounts payable subsidiary ledger,

- Investors subsidiary ledger,

- Employees subsidiary ledger,

- Tenants subsidiary ledger.

Advantages of Subsidiary Ledger

Subsidiary ledgers have several advantages. Such of them are as follows:

- It provides the up-to-date information on specific account balances.

- It shows transactions affecting one customer or one creditor in a single

- It makes easy to free the general ledger of excessive details.

- It minimizes the number of accounts for making an easy trial balance.

- It helps to locate errors in individual accounts using control accounts.

- It makes possible a division of labour in posting.

In short, subsidiary ledger ensures that account information is current.