Segment Margin differs from Contribution Margin

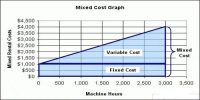

Contribution margin is the amount remaining from sales revenue once all variable costs have been removed. Contribution margin ratio is commonly expressed as a percentage of sales prices. It is the difference between a company’s sales and variable expenses, expressed as a percentage.

i.e., Contribution Margin = Sales Revenue – Variable Costs

Segment margin is the margin available after a segment has covered all of its costs. It’s one of the best ways to determine the long-term profitability of a segment. It is the amount of net profit or net loss generated by a portion of a business. It can be useful for determining the vulnerability of a company’s overall gross margins.

i.e., Segment Margin = Segment’s Contribution Margin – Fixed Costs traced to the Segment

Segment margin is a measure of profitability that applies to individual product lines. It is calculated as segment revenues minus variable costs minus avoidable fixed costs. Segment margin is used to measure the profitability of a segment or product line when making the decision of whether to continue or discontinue that segment or product line. To calculate the contribution margin that is used in the numerator in the preceding calculation, subtract all variable costs from revenues. So, the contribution margin ratio is the percentage of revenues that are available to cover a company’s fixed costs, fixed expenses, and profit.