Subsidiary book is the subdivision of the Journal. In these books, the details of the transactions are recorded as they take place from day to day in a classified manner.

Purpose of Subsidiary Books

Subsidiary book is the subdivision of the Journal. These are known as books of major entry or books of unique entry as all the dealings are recorded in their unique form. In these books, the details of the transactions are recorded as they take place from day to day in a confidential method

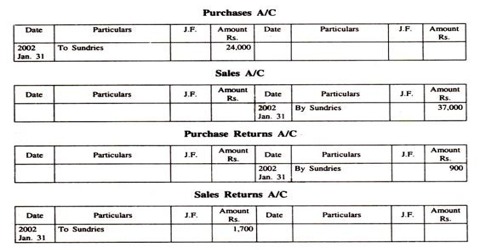

- Purchases Book records only credit purchases of goods by the trader. They are used to record all the credit purchases.

- Cash Book Used to record all the cash receipts and payments.

- Sales Book is meant for entering only credit sales of goods by the trader. They are used to record all the credit sales

- Purchases Return Book records the goods returned by the trader to suppliers.

- Sales Return Book deals with goods returned (out of previous sales) by the customers. They are used to record all goods returned by the customer to the business.

- Bills Receivable Book records the receipts of bills (Bills Receivable). They are used to record all accepted bills received by the business.

- Bills Payable Book records the issue of bills (Bills Payable). They are used to record all bills accepted by us to our creditors.

- Cash Book is used for recording only cash transactions i.e., receipts and payments of cash.

- Journal Proper is the journal that records the entries which cannot be entered in any of the above-listed subsidiary books. They are used to record those transactions for which there is no separate book.

These books record the details of the transactions and therefore facilitate the ledger to become brief. Future reference and any preferred analysis become simple as transactions of comparable nature are recorded jointly.

Advantages

Saving Labor Hours: Recording in a subsidiary book saves a lot of time and clerical hours. This helps reduce the time it takes to totally record a transaction.

Division of Work: In place of one general journal, we have several subsidiary books. This will save time, improve efficiency and result in fewer errors as well.

Specialization of Work: If one person maintains the same subsidiary book over many years he acquires full knowledge and understanding of the work.

Easy for Reference: Whenever any information is needed we directly refer the subsidiary book to get said information.

Easier for Checking: If the Trial Balance does not match, it will be much easier to locate the error thanks to the existence of separate books i.e. a subsidiary book.