Return on capital employed ratio is calculated by dividing the net income before interest and tax by capital employed. It measures the success of a business in making satisfactory profit on capital invested. This ratio is stated in percentage.

Formula

The general components of the formula of return on capital employed ratio are net income before interest and tax and capital employed.

Net income before interest and tax (Operating income):

Net profit before the deduction of interest and tax expenses is offensively called operating income. Below, interest means interest on lasting loans. If organization pays interest costs on short-term borrowings, which is deducted to reach operating income.

Capital employed:

Capital employed is calculated in a number of ways. Some popular methods are given below:

- Total of fixed and current assets.

- Total of fixed assets only.

- Fixed assets plus working capital.

- Total of long term funds. Long term funds include capital, Reserve and surplus etc.

In managerial accounting, the last method is usually used to calculate capital employed.

Expense:

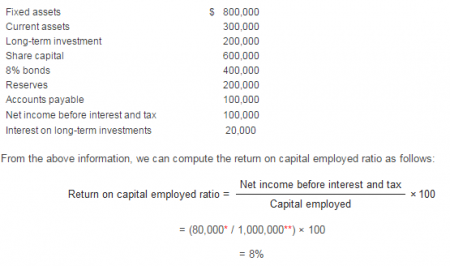

Computation of net profit before interest and tax:

Net income before interest and tax – Interest on long term investment

= $100,000 – $20,000 = $80,000

Computation of capital employed:

Fixed assets + Current assets – Current liabilities

= $800,000 + $300,000 – $100,000 = $1,000,000

Significance and Interpretation:

Return on capital employed ratio measures the effectiveness with how the investment made by means of shareholders and loan companies is used in the industry. Managers use this specific ratio for different financial decisions. This is a ratio of overall profitability plus a higher ratio is, therefor, better.

To determine whether the business has improved it is profitability or not necessarily, the ratio is usually calculated for assorted years.