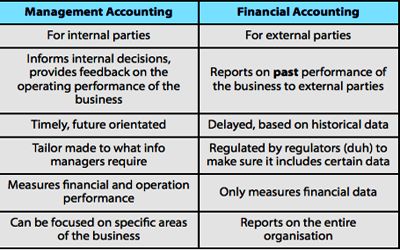

Main distinctions between Financial and Management Accounting

Financial Accounting

- The main objective of financial accounting is to measure business income and communication of business information to the various categories of persons like management, creditors, suppliers, bankers, investors etc.

- Financial accounting focuses on history; reports on the prior quarter or year.

- Financial accounting has its focus on the financial statements which are distributed to stockholders, lenders, financial analysts, and others outside of the company.

- The financial accounting deals with all the activities of the business, assesses results of the business as a whole and reveals the overall performance and position of the enterprise.

- Financial accounting lays emphasis on the past activities and represents historical records.

- Financial accounting records the transactions relating to income, expenses, revenue, personal accounts.

- Financial accounting reports on the results of an entire business.

- Financial accounting is concerned with the financial results that a business has already achieved, so it has a historical orientation.

Management Accounting

- The main objective of management accounting is to help the internal management.

- Managerial accounting focuses on the present and forecasts for the future.

- Managerial accounting has its focus on providing information within the company so that its management can operate the company more effectively.

- Management accounting is limited in its coverage. Management accounting concerns with the activities of the different units, departments or divisions and deals with significant activities of the business.

- Management accounting stresses the future and uses historical costs and data for estimating the future.

- Management accounting reports costs and revenue by profit center or responsibility center.

- Managerial accounting almost always reports at a more detailed level, such as profits by product, product line, customer, and geographic region.

- Managerial accounting may address budgets and forecasts, and so can have a future orientation.