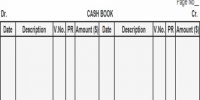

The single entry method is a partial structure of demo financial transactions. It is the method, which has no permanent set of rules to documentation the financial transactions of the trade only single entry is recorded which can be each debit or credit business deal. It does not require hiring skilled accounting personnel to record financial transactions of the business. Further, it does not require a large number of books to record a limited number of financial transactions.

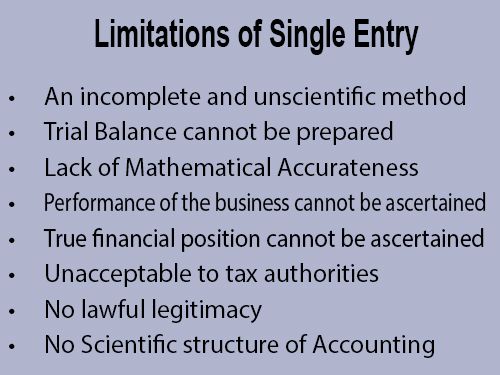

Limitations of Single Entry:

Under this method, an only fractional and shortened record is maintained because twofold aspects of transactions are normally ignored. As the twofold aspects of each transaction are not recorded, a trial balance cannot be drawn up to test the mathematical correctness of the records.

- An incomplete and unscientific method

This system is incomplete because real and nominal accounts are not prepared and also due to the fact that the debt and credit aspect of all transactions are not recorded.

- Trial Balance cannot be prepared

Quite often this system does not record both the aspects of transactions, therefore, at the end of the year, arithmetical accuracy of the books cannot be checked by preparing a trial balance.

- Lack of Mathematical Accurateness

There is no record of balances of accounts because we do not make ledger. In other words, there is a big possibility of arithmetical errors and mistakes in this method.

- Performance of the business cannot be ascertained

Trading, profit and loss account cannot be prepared and hence the gross profit, net profit, and rate of net profit on sales cannot be known.

- True financial position cannot be ascertained

It is very difficult to prepare a balance sheet, so the true financial position cannot be ascertained.

- Comparison with previous years performance is not possible

Due to incomplete information and the non-availability of previous years’ information, a comparison between the current and previous years’ performance cannot be made. A comparison is required to identify the areas of weakness and rectification.

- Unacceptable to tax authorities

Tax authorities (income tax and sales tax) do not accept accounts prepared according to a single entry system for computation of taxes.

- Difficulty in obtaining a loan

Accounts prepared according to this system are not accepted by banks and other money lending institutions, so it is very difficult to obtain a loan.

- Difficult to locate frauds

It is difficult to locate frauds under this system and so employees may become dishonest and negligent. It encourages misappropriation, fraud, and carelessness.

- No lawful legitimacy

Accounting records that are made under a single entry system are not accepted by law. Because we do not verify these records under scientific rules of accounting.

- No apply for verdict Financial Position

Without knowing the existing financial situation, doing business is an immense risk. So, all those who are using a single-entry system are doing business under immense danger of loss of capital.

- Difficult to determine the price of the business

Due to the absence of true and reliable net profit or assets and liabilities, it is difficult to determine the price of the business at the time of its sale.

- No Scientific structure of Accounting

Instead of using this, a business organization should use the double-entry system of accounting which is fully scientific under accounting standards.

The single entry system is an economical system of recording financial transactions. On the basis of the previous explanation of the limitation of single entry system, it is feasible to specify its particular limitations are:

- Complete information about the business record or transaction cannot be obtained because partial records are maintained.

- The mathematical correctness of the accounts cannot be justified in the absence of Double Entry.

- In the lack of mathematical analysis, the threat of fraud and mistakes and their non-discovery is enlarged.

- It is not doable to arrange a Profit and Loss Account as nominal accounts are not preserved and so the basis of profit or loss cannot be determined.

- A Balance Sheet cannot be maintained, so, the accurate financial situation cannot be identified.

- Because of arithmetical data are not maintained, so assessment of business from year to year is not feasible.

- Errors and mistakes are relatively frequent. If it has happened cannot be traced out simply.

- A counter check is not at all doable, as in Double Entry System.