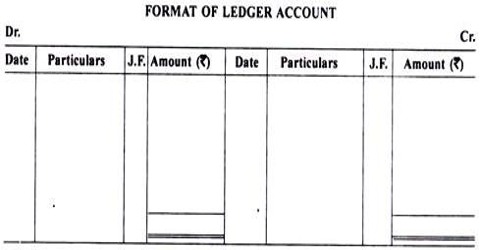

Format of Ledger

A Ledger is a book that includes all the accounts whether individual, real or nominal, which is primary entered in a journal or particular reason subsidiary books. Ledger serves as the main book for an effective and result oriented accounting system. In computerized systems, it consists of interlinked digital files but follows the same accounting principles as the manual system. It is a collection of all accounts, debited or credited in the books of original entry viz. subsidiary books and proper journal. Here briefly explain the simple format of the ledger.

- Each ledger account is divided into two parts. The left-hand side is known as the debit side and the right-hand side is known as the credit side. The words ‘Dr.’ and ‘Cr.’ are used to denote Debit and Credit.

- The name of the account is mentioned in the top (middle) of the account.

- The date of the transaction is recorded in the date column.

- The word ‘To’ is used before the accounts which appear on the debit side of an account in the particulars column. Similarly, the word ‘By’ is used before the accounts which appear on the credit side of an account in the particulars column.

- The name of the other account which is affected by the transaction is written either in the debit side or credit side in the particulars column.

- The page number of the Journal or Subsidiary Book from where that particular entry is transferred is entered in the Journal Folio (J.F) column.

- The amount pertaining to this account is entered in the amount column.

Rules for writing Journal Entries in Ledger Account –

Liabilities: this decreases on the side of debt and increases on the credit side.

Assets: In assets, the figure increases on the left side or you can say the debit side. While this decreases on the credit side or the right side.

Capitals: This follows the same rule as liabilities.

Gains or Income: In this, there is a decrease on the debit side. Also, there is an increase in the credit side.

Expenses: The expenses in the ledger decrease on the credit side while increases on the debit side.

How to Write and Prepare Ledger Account –

- Drawing the Form – Get pen and paper, start drawing the ledger account. The left side of it is the debit side and the right side is the credit side.

- Posting transactions from journal to respective ledger account. A debit account of the journal is posted on the debit side of that account and the credit account of the journal is posted on the credit side of that account.

- Folioing – Put the page number for a journal entry on the ledger account’s folio column.

- Casting – Separating debit and credit amount. In this way totaling of debit and credit is called casting.

- Balancing – find the difference between debit and credit to get debit or credit balance of the account. Thereafter the amount of difference is added in the deficit side to equalize both sides. This sort of difference between the two sides of accounts is called balance.