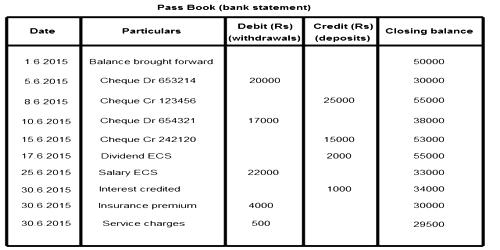

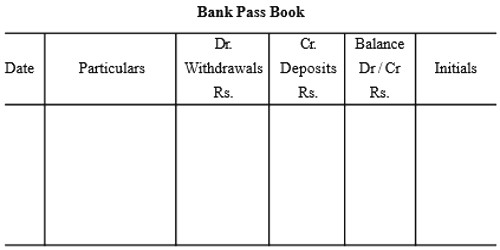

Format of Bank Pass Book

Passbook is an essential document nearly all of us have. Bank Pass Book is a duplicate of the account of the client as it appears in the bank’s books. When a client deposits money and cheques into his bank account or withdraws money, he records these transactions in the bank column of his cashbook instantly. Its key function is to proceed as a conclusive record of banking transactions between the customer and the banker.

The bank gives to its clients such a passbook or a statement of account. This Passbook is abounding by the bank to its every client who opens an account. This book records all deposits and withdrawals. Correspondingly, the bank records them in the customer’s account maintained in its books. Then they are copied in a passbook and given to the customer.

In the date column, the dates of the transactions are recorded. In the particulars column withdrawals and deposits are recorded. The balance after each transaction is recorded in the next column and the bank official signs in the last column.

Following the principles of Double Entry, banker credits the account of the customer for all the amounts received from the customer and on his behalf. Similarly, the banker debits the account of the customer for all withdrawals and amounts paid to others on behalf of the customers.

The main point to be remembered is that entries are made only after cash is received or paid, except in the case of interest and bank charges. Interest and bank charges are mere book adjustments and in these, there is neither receipt of cash nor payment of cash.

Sample Format of a Bank Passbook or Bank Statement:

- Name of the bank: … … …

- Address of the bank: … … …

- Account No.: … … …

- Customer Name: … … …

- Address of the customer: … … …

Thus passbook is a record of the banking transactions of a client with a bank. All entries made by a client in his cashbook (bank column) must be entered by the bank in the passbook.