Differentiate between Absorption and Variable Costing

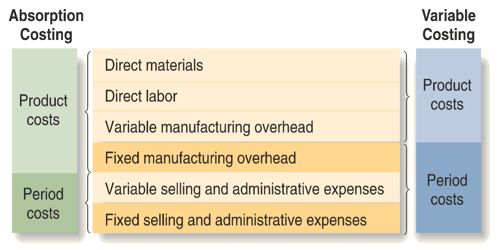

Absorption Costing means that all of the manufacturing costs are absorbed by the units produced. In other words, the cost of a finished unit in inventory will include direct materials, direct labor, and both variable and fixed manufacturing overhead. Variable Costing is a managerial accounting cost concept. Under this method, manufacturing overhead is incurred in the period that a product is produced. The differences between absorption costing and variable/direct costing are as follows –

Absorption costing

- Absorption, the cost is the practice of charging all costs, both fixed and variable to operations, process, or products.

- Fixed manufacturing overhead is treated as a product cost and is an asset until products are sold.

- It includes direct materials, direct labor and both variable and fixed manufacturing overhead in the cost of a unit of product.

- Under the full costing method, fixed manufacturing overhead costs are expensed when the product is sold.

Variable/direct costing

- In variable costing, only manufacturing costs are assigned to units cost.

- Fixed manufacturing overhead is treated as a period cost and is deducted in full from the current period’s revenue.

- It includes direct materials, direct labor and variable manufacturing overhead in the cost of a unit of product.

- Under the direct costing method, fixed manufacturing overhead costs are expensed during the period in which they are incurred.