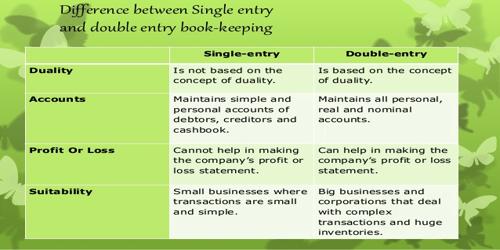

Differences between Double Entry System and Single Entry System

Single Entry System is an incomplete, incorrect, unscientific and haphazard method of book keeping. The name of the system itself shows that the double aspects of business transactions are not recorded.

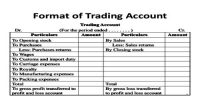

The double entry system of accounting means that each trade transaction will engage two accounts (or more). In short, the essential principle of this system is, for every debit, there must be a corresponding credit of equal amount and for every credit, there must be a corresponding debit of equal amount

Double Entry System

- Principle: For every debit, there is a corresponding credit and vice versa

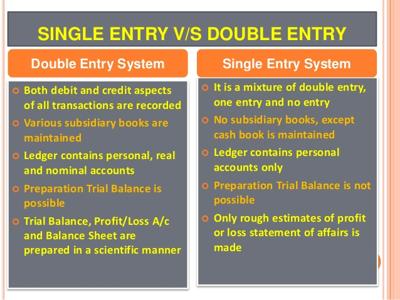

- Recording of transaction: Debit and credit aspects of all transactions are recorded.

- Nature of accounts maintained: Maintains the complete record of personal, real and nominal accounts.

- Trial Balance: Arithmetical accuracy of the records can be checked by preparing a Trial Balance.

- Determination of profit or loss and financial position: A Profit and Loss Account and Balance sheet can be conveniently prepared since the book of accounts present a complete picture.

- Suitability: It is suitable for all types of traders.

- Dependability: It is the only scientific system of keeping books of accounts.

- Acceptability: Records are acceptable for the purpose of tax, loans etc.

- Internal check: Internal check is possible.

Single Entry System

- Principle: Debit and credits do not agree.

- Recording of transaction: Debit and credit aspects of all transactions are not recorded.

- Nature of accounts maintained: An incomplete record. Only personal and cash accounts are maintained.

- Trial Balance: Trial Balance cannot be prepared.

- Determination of profit or loss and financial position: A Profit & Loss Account and Balance sheet cannot be conveniently prepared since the accounting records are incomplete.

- Suitability: It is suitable for only small traders.

- Dependability: It is not a system. It is incomplete and unscientific.

- Acceptability: Records are not acceptable for the purpose of tax claims, loans etc.

- Internal check: Internal check is not possible.