Source Documents for the recording of transactions

Source documents are the proofs of business transactions which present information about the nature of the transaction, the date, the amount and the parties involved in it. So, it is the imaginative record including the information to authenticate a transaction entered into an accounting system.

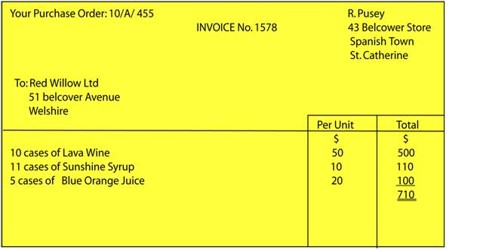

For example, a company’s source document for the recording of merchandise purchased is the supplier’s invoice supported by the company’s purchase order and receiving the ticket.

Transactions are recorded in the books of accounts when they, in fact, take place and are suitably supported by source documents. According to the supportable objective principle of Accounting, each transaction recorded in the books of accounts should have sufficient evidence to maintain it. These supporting documents are the written and genuine evidence of the accuracy of the recorded transactions. These documents are required for audit and tax evaluation. They also serve as the lawful evidence in case of a disagreement.

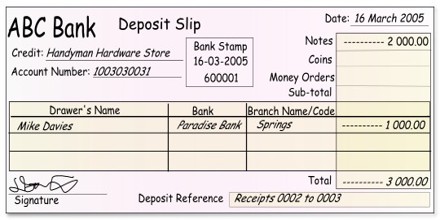

The following are the most common source documents.