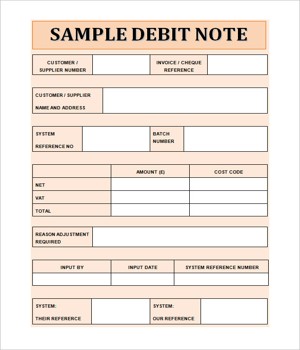

Debit Note is a document which reflects that a debit is made to the other party’s account. It is prepared by the purchaser and it includes the time of the goods returned, name of the supplier, details of the goods returned and reasons for returning the goods. Debit Note is issued by the buyer, at the time of returning the goods to the vendor. Each debit note is in sequence numbered. A replica copy or counter foil of the debit note is retained by the buyer. On the source of debit note, the suppliers account is debited in the books.

Debit notes are raised in cases where there is a tax invoice issued, but the taxable value of the goods therein changes after such issuance. Correspondingly, there can be a tax invoice issued but a number of tax changes after such issuance. In both these cases, a seller has to intimate the purchaser about such change.

Few Characteristics of a Debit Note

- It is sent to inform about the debit made in the account of the seller along with the reasons mentioned in it.

- The purchase returns the book is updated on its basis.

- It is regularly used to return goods on credit.

- It is usually arranged like a customary invoice and shows a positive amount.

There is no particular design to issue a debit note, but it can be issued as a letter or a formal document. It is regularly a document specifying future accountability and having business implications. They enlarge the credit period of a transaction, but are affected after shipping of goods takes place.