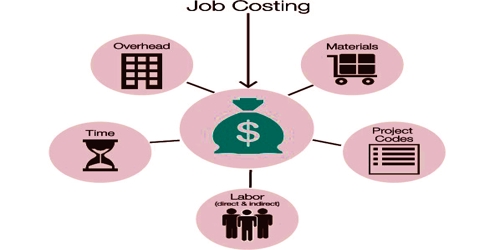

Job costing is one of the methods of costing. It is also known as job order costing. In this system, work is undertaken to customer’s specific requirements on the basis of orders.

Characteristics of Job Order Costing –

(a) A job consists of a single order or contract.

(b) It is a cost unit by itself.

(c) Each job is unique in nature.

(d) Products are not manufactured for general-consumption.

(e) Under job costing, the cost of each job is ascertained after the completion of the job.

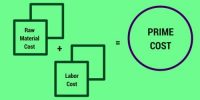

(f) The costs of each job are ascertained by adding materials, labor, and overheads.

(g) Each order is given a job number.

(h) Costs are accumulated with reference to this number.

(i) Costs are ascertained for each order.

(j) Generally, the duration of the job order is comparatively short (products).

(k) Work-in-progress may or may not exist at the end of the accounting period.

(l) An important feature of job costing is that it is possible to identify a job at each stage of its manufacturing process.

(m) By comparing the actual cost of each job against the price charged for each job, the profit or loss made on each job is ascertained.

(n) Under this method, the cost of each job and the profit or loss made on each job undertaken is found out separately.

In job costing, it is not necessary that each job will flow through all the production cost centers in a predetermined manner. The purpose of job costing is to bring together all the costs incurred for completing a job. The industries need not to incur selling and distribution expenses as the customers themselves come to place orders and collect the goods after production.