Causes of Under and Over Absorption of Overhead

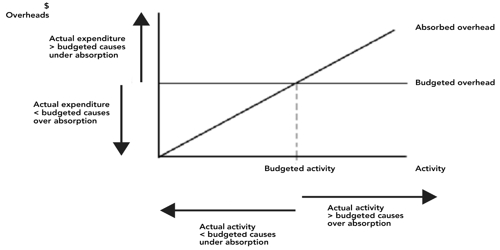

Under absorbed factory overheads: this situation arises if the overheads absorbed are less than the actual overheads. It arises when the amount of overhead that has been incurred exceeds the amount of overhead that has been absorbed. It is also termed as ‘under-recovery’. Following factors would create tinder absorbed factory overheads:

- Actual overheads being more than the estimated overheads,

- The actual output is less than those estimated.

For example; if the overheads absorbed on a predetermined basis are $ 10,000 and the actual overheads incurred are $ 12,000, there is under-absorption to the extent of $ 2000.

Over absorbed factory overheads: this situation arises if the overheads absorbed are more than the actual overheads. It arises when the amount of overhead that has been absorbed exceeds the amount of overhead that has been incurred. Following factors would create over absorbed factory overheads:

- Actual overheads being less than the estimated overheads,

- The actual output is more than the estimated.

For example, the overheads recovered are $ 30,000 and the actual production overheads are $ 27,500 then there will be over-absorption of $ 2500. ($30,000 – $27,500).

Methods for disposal of under or over-absorption of factory overheads:

- Apportionment through supplementary rates.

- Transfer to Costing Profit and Loss Account

- Carryover to next year’s Accounts.

When the actual output considerably differs from the probable output, it leads to under or over-absorption of overheads. When the cause is abnormal the amount of under or over-absorption should be treated as an abnormal loss and transferred to costing profit and loss accent.